The Best and Cheapest Homeowners Insurance in Montana (2025)

State Farm sells the best homeowners insurance in Montana, with rates averaging $1,930 per year for $350,000 in dwelling coverage.

Compare Home Insurance Quotes in Montana

Best Cheap Home Insurance in Montana

To find the best homeowners insurance in Montana, ValuePenguin's experts reviewed rates, coverage, discounts and customer service for the biggest insurance companies in Montana. See the full methodology.

Cheapest home insurance companies in Montana

State Farm has the cheapest homeowners insurance in Montana for most people.

A State Farm policy costs an average of $1,930 per year for $350,000 in dwelling coverage. That's $560 per year cheaper than the state average. Nationwide also has cheap rates for most homes. But if you need a policy with $500,000 or $1 million in coverage, Chubb is a cheaper option.

Find Cheap Home Insurance Quotes in Montana

Home insurance in Montana is 16% more expensive than the national average cost of home insurance, which is $2,151 per year.

Cheap home insurance in Montana

$200,000

$350,000

$500,000

$1 million

Company | Annual rate | ||

|---|---|---|---|

| State Farm | $1,355 | |

| Nationwide | $1,523 | |

| Farmers | $1,685 | |

| USAA | $2,014 | |

| Allstate | $2,806 | |

$200,000

Company | Annual rate | ||

|---|---|---|---|

|

| State Farm | $1,355 | |

|

| Nationwide | $1,523 | |

|

| Farmers | $1,685 | |

|

| USAA | $2,014 | |

|

| Allstate | $2,806 | |

$350,000

Company | Annual rate | ||

|---|---|---|---|

|

| State Farm | $1,930 | |

|

| Nationwide | $2,432 | |

|

| Farmers | $2,509 | |

|

| USAA | $2,744 | |

|

| Allstate | $3,737 | |

$500,000

Company | Annual rate | ||

|---|---|---|---|

| Chubb | $2,053 | |

|

| State Farm | $2,552 | |

|

| USAA | $3,293 | |

|

| Farmers | $3,411 | |

|

| Nationwide | $3,554 | |

$1 million

Company | Annual rate | ||

|---|---|---|---|

|

| Chubb | $3,625 | |

|

| State Farm | $4,437 | |

|

| USAA | $4,853 | |

|

| Farmers | $5,283 | |

|

| Allstate | $7,025 | |

What home insurance coverage do you need in Montana?

Homes in Montana might have to withstand wind, hail, wildfires and floods. Home insurance usually covers damage caused by extreme weather, but you need separate flood insurance for flood damage.

Best home insurance in Montana for most people: State Farm

-

Editor's rating

- Cost: $1,930/yr

State Farm has cheap rates and local agents for advice, making it best for most people.

Pros:

-

Cheap rates

-

Local agents available

-

Great for bundling with car insurance

Cons:

-

Fewer discounts and coverages than some companies

-

Average customer service

-

Can't buy a policy online

State Farm's low rates for home insurance make it the best option for most people. Montana home insurance from State Farm costs $1,930 per year for a policy with $350,000 in dwelling coverage, the cheapest rate in the state.

State Farm has agents in 43 Montana cities. An agent can help you choose the right insurance for your needs. With State Farm, though, you have to work with a local agent to buy a policy. You can get quotes online, but you can't finalize and buy your insurance without talking to an agent.

State Farm also has the cheapest car insurance in Montana, so it's great for bundling your policies. Full coverage costs $141 per month. That's $40 cheaper than the state average of $181.

However, State Farm's customer service is only average. The company has 5% more complaints about its home insurance than expected for a company its size. And the company doesn't offer as many coverages or discounts as some companies. If you want to personalize your policy, Nationwide is a better option.

Best home insurance in Montana for extra coverage: Nationwide

-

Editor's rating

- Cost: $2,432/yr

Nationwide has plenty of coverage options to personalize your policy.

Pros:

-

Lots of coverage options and discounts

-

Cheap rates

-

Local agents available

Cons:

-

Average customer service

Nationwide is a good option if you have specific needs or want to personalize your home insurance. The company has a long list of extra coverage options, including coverage for identity theft, earthquakes and water backing up into your home.

One of Nationwide's most impressive coverage options is "Better Roof Replacement." If your roof is damaged and you have this coverage, Nationwide will pay to replace it with stronger roofing materials.

Nationwide also has several discounts to help you lower your rate. You can save if you bought your home within the last 12 months, if you live in a gated community, and if you've updated your home's plumbing, electrical, heating or cooling systems.

Nationwide's customer service is just average, though. The company gets 4% fewer complaints about its home insurance than an average company its size. But J.D. Power ranked Nationwide below average in its 2023 Home Insurance Study.

Best home insurance in Montana for expensive homes: Chubb

-

Editor's rating

- Cost: $2,053/yr

Chubb has cheap rates for high-value and luxury homes.

Pros:

-

Cheap rates for luxury homes

-

Excellent customer service

-

Coverage tailored to high-value homes

Cons:

-

Only available for high-value homes

-

No online quotes

-

Not many agents in MT

Chubb has cheap rates and policies specifically for high-value homes. The company has tools that work to prevent damage before it happens. Chubb's "HomeScan" uses infrared light to check your home for faulty wiring, missing insulation and leaks. This lets you fix an issue before it causes damage.

With the Chubb "Masterpiece" policy, a professional will come to your home to help you decide what types of damages are most likely to happen. Then, they'll help you choose your coverage to fit your specific needs. This might be part of why Chubb also has excellent customer service, with 89% fewer complaints than expected for a company its size.

You won't be able to get Chubb coverage if your home is worth less than $500,000. And you can't get quotes or buy a policy online with Chubb. You have to work with an agent to even get a quote. And unfortunately, Chubb doesn't have many agents in Montana. If you don't live near a Chubb agent, you'll have to get your quote and buy a policy over the phone.

What's the average cost of home insurance in Montana?

In Montana, you'll pay an average of $2,490 per year for a policy with $350,000 of dwelling coverage.

That's more expensive than in Idaho and Wyoming, where the same coverage costs $1,437 per year and $1,932 per year, respectively. That's probably because homes in Montana are more likely to be damaged by severe weather.

Rates in North and South Dakota are closer to Montana's rates, though. A policy with $350,000 in dwelling coverage costs $2,372 per year in North Dakota and $2,596 per year in South Dakota.

Average cost of home insurance in Montana by dwelling amount

Dwelling coverage | Annual cost |

|---|---|

| $200,000 | $1,753 |

| $350,000 | $2,490 |

| $500,000 | $3,218 |

| $1,000,000 | $5,497 |

No matter where you live, you'll pay more for home insurance if you need more coverage. Expensive homes cost more to repair after they're damaged, so insurance companies charge higher rates to make up for the risk of expensive claims.

Montana home insurance rates by city

Columbia Falls, near Flathead National Forest in northwestern Montana, has the cheapest home insurance in the state.

A policy with $350,000 in dwelling coverage costs $1,603 per year in Columbia Falls. That is 36% cheaper than the state average. Baker, Montana, on the eastern side of the state near the border with North Dakota, has the highest rates for home insurance, averaging $3,624 per year.

City | Annual rate | % from avg. |

|---|---|---|

| Absarokee | $2,662 | 7% |

| Acton | $2,937 | 18% |

| Alberton | $1,804 | -28% |

| Alder | $2,129 | -14% |

| Alzada | $3,484 | 40% |

Rates are for a policy with $350,000 of dwelling coverage.

Best-rated homeowners insurance companies in Montana

USAA is the best home insurance company in Montana because of its great service.

USAA has fewer than half the complaints expected for a company its size and excellent coverage. But you can only get USAA if you're a military member, veteran or qualifying family member. For most people, State Farm is the best option.

Company |

Rating

|

Complaints

|

|---|---|---|

| USAA | Low | |

| State Farm | Average | |

| Chubb | Average | |

| Allstate | Average | |

| Nationwide | Average |

What kind of home insurance should you get in Montana?

Montana homes have to endure severe weather, such as extreme temperatures, heavy snow, high winds, wildfires and floods. Home insurance usually covers most types of damage, except damage from floods, but you should check with your agent to make sure.

Does homeowners insurance in Montana cover hail and wind damage?

Home insurance usually covers damage from hailstorms and windstorms. You might have to pay a separate wind and hail deductible, which is usually higher than your normal deductible. Review your policy or talk to your insurance company to find out how much your wind/hail deductible is, if you have one.

Montana had 135 windstorms and 75 hailstorms in 2023. Storms like this can damage your roof and siding, which can lead to water damage inside your home when it rains. Make sure your roof and siding are in good condition because home insurance might not cover you if your house is not well maintained.

Does Montana home insurance cover wildfires?

Most home insurance policies cover damage caused by wildfires. If you're in a particularly high-risk area, you might have limited coverage, though, or you may need to get a separate policy. Talk to your insurance company before a fire happens to make sure you're covered.

Montana experienced 1,662 fires in 2023, which burned over 123,000 acres of land. More than 1,200 of those fires were started by humans. To help lower your home's risk of catching on fire, consider getting a fire-resistant roof, installing window coverings and creating a barrier of rock around your home.

Does homeowners insurance in Montana cover floods?

Home insurance doesn't cover floods. You have to buy a separate flood insurance policy to have coverage. Your home insurance company might be able to help you get coverage from the National Flood Insurance Program (NFIP). Or you might be able to find a private company that offers its own policies.

True floods happen when an area that is normally dry is underwater. This can happen after heavy rains or when snow melts. Nearly every county in Montana has had flooding since the early 1950s, when records began. Even if you're not in a high-risk area, it's smart to get a quote for flood insurance.

How to save on Montana home insurance

Montana's home insurance rates can be expensive, but there are some ways you can lower your price.

Shop around. Comparing home insurance quotes lets you see what company has the cheapest rates for the coverage you need. It also lets you find a company with good service and discounts you qualify for.

Ask about discounts. Home insurance discounts, like a discount for bundling your policy with your car insurance, can also help you lower your rate. You can also usually save for having a home alarm system, staying with the same company for several years and not smoking.

Replace your roof. Montana's weather can be hard on roofs. Getting a new roof that is wind- and fire-resistant might earn you a discount on your policy. New roofs are also less likely to get damaged, which means you might file fewer claims.

Maintain your home. A home that is in good condition is less likely to be damaged by Montana's harsh weather, which keeps you from filing claims. This won't make your rate lower immediately, but it'll help keep it from going up so much over time.

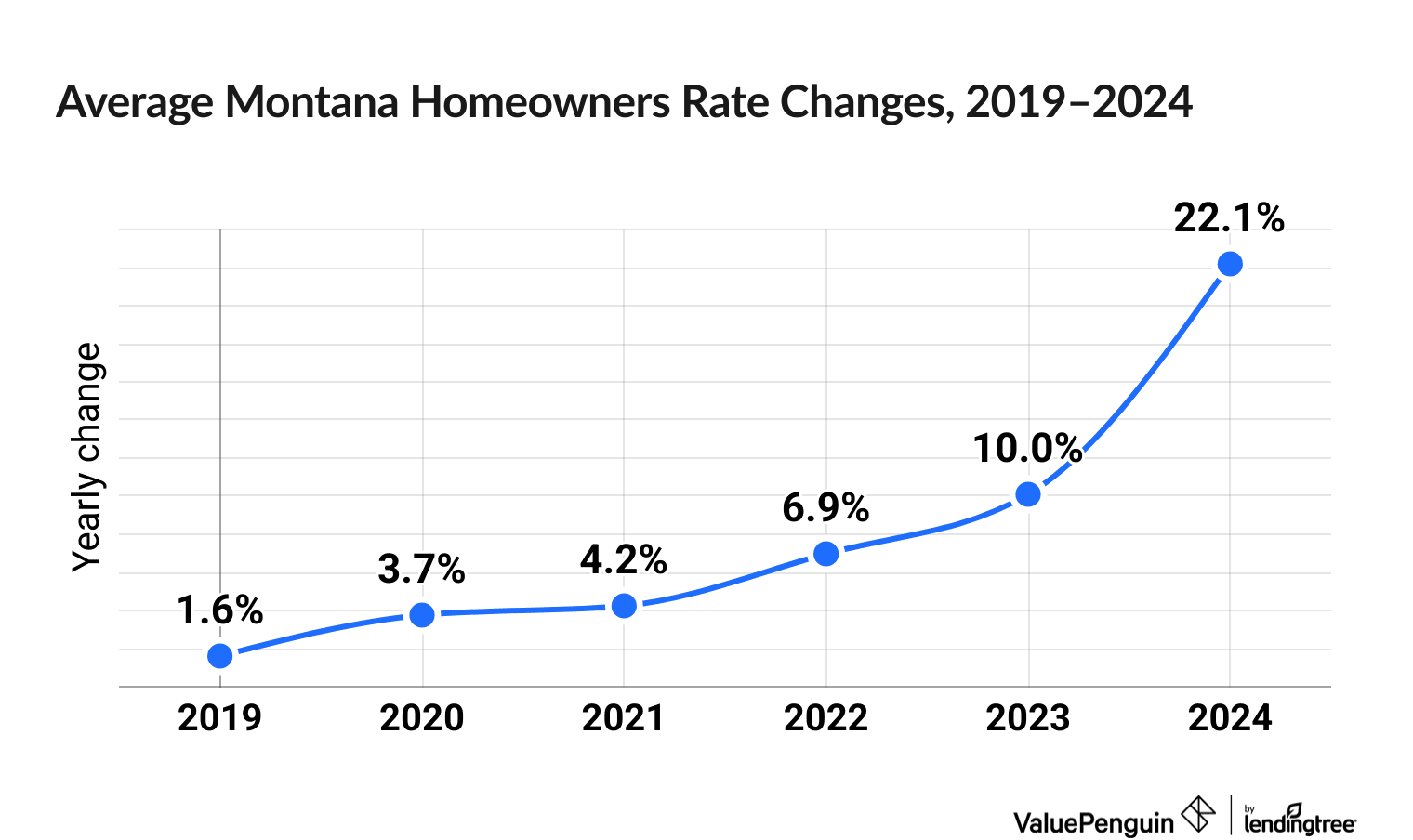

Surging Montana home insurance costs

Home insurance prices are up 57.8% in Montana over the last six years.

Montana homeowners have seen a sharp rise in their home insurance prices in recent years, experiencing an increase of 10.0% in 2023 followed by a 22.1% increase in 2024.

Home insurance costs at Travelers increased the most during the past six years, at 80.2%. Following closely behind was Liberty Mutual with a 78.9% increase, and Farmers Insurance, at 77.9%.

Home insurance rate change data was compiled using RateWatch from S&P Global, which uses information from the National Association of Insurance Commissioners (NAIC).

Frequently asked questions

How much is homeowners insurance in Montana?

Home insurance in Montana costs an average of $2,490 per year for a policy with $350,000 in dwelling coverage. The amount you pay will depend on where you live in Montana, how much coverage you need, if you've filed any home insurance claims before and more.

Who has the best homeowners insurance in Montana?

USAA has the best-rated home insurance in Montana, but you can only get it if you're a veteran, military member or family member. For most people, State Farm is the best choice. If you have a high-value home, Chubb is the best option.

Is homeowners insurance required in Montana?

No, the state of Montana does not require anyone to buy home insurance. But if you have a mortgage, your bank will require you to have a policy. If you don't have a mortgage, you can technically go without home insurance, but it's not usually a good idea unless you can easily afford to repair or rebuild your home yourself.

Methodology

To find the cheapest home insurance in Montana, ValuePenguin got quotes from the largest home insurance companies in every ZIP code in Montana. The quotes are for a 45-year-old married man with good credit, no claims and the following coverage limits:

- Dwelling coverage: $200,000, $350,000, $500,000 or $1 million

- Personal liability: $100,000

- Medical payments: $5,000

- Deductible: $1,000

The home insurance rates featured in this article are from Quadrant Information Services. Quadrant uses publicly sourced insurance rate filings in its database. The rates in this article are for comparison purposes only. Your home insurance quotes will be different and based on your unique situation.

ValuePenguin chose the best home insurance in Montana by reviewing each company's rates, customer complaint data from the National Association of Insurance Commissioners (NAIC) and scores from J.D. Power's home insurance customer satisfaction survey. Our experts also looked at each company's coverage options and discounts.

Other sources include the Federal Emergency Management Agency (FEMA), the National Interagency Coordination Center annual wildfire report and the Storm Prediction Center.

Editorial Note: The content of this article is based on the author's opinions and recommendations alone. It has not been previewed, commissioned or otherwise endorsed by any of our network partners.