State of Auto Insurance in 2025

Car insurance prices are expected to increase an average of 7.5% in 2025.

That's a significant slowdown from the past two years, when car insurance rates rose an average of 16.5% in 2024 and 12.0% in 2023.

The average cost of car insurance nationwide in 2025 is $175 per month for full coverage. Nevada, Florida and Michigan are the most expensive states in the U.S. for car insurance, all with prices exceeding $250 per month.

How much does car insurance cost in my state?

The average cost of full coverage car insurance for 2025 is $2,101 per year, or about $175 per month.

The most expensive states for full coverage car insurance are Nevada ($286 per month), Florida ($272) and Michigan ($263). These three states are all 50% more expensive than the national average rate of $175 per month.

Car insurance prices vary dramatically by state, with coverage in the most expensive states being at least 2.5 times as much as the cheapest states.

The three states with the cheapest car insurance barely crack $100 per month for the same policy. Maine drivers pay an average of just $103 per month, while neighboring New Hampshire and Vermont are tied at $107 per month — all for the same level of coverage.

Those prices are about 40% below the national average.

Car insurance costs by state

State | Avg monthly rate | % from average |

|---|---|---|

| Nevada | $286 | 64% |

| Florida | $272 | 56% |

| Michigan | $263 | 50% |

| Louisiana | $249 | 42% |

| Colorado | $241 | 38% |

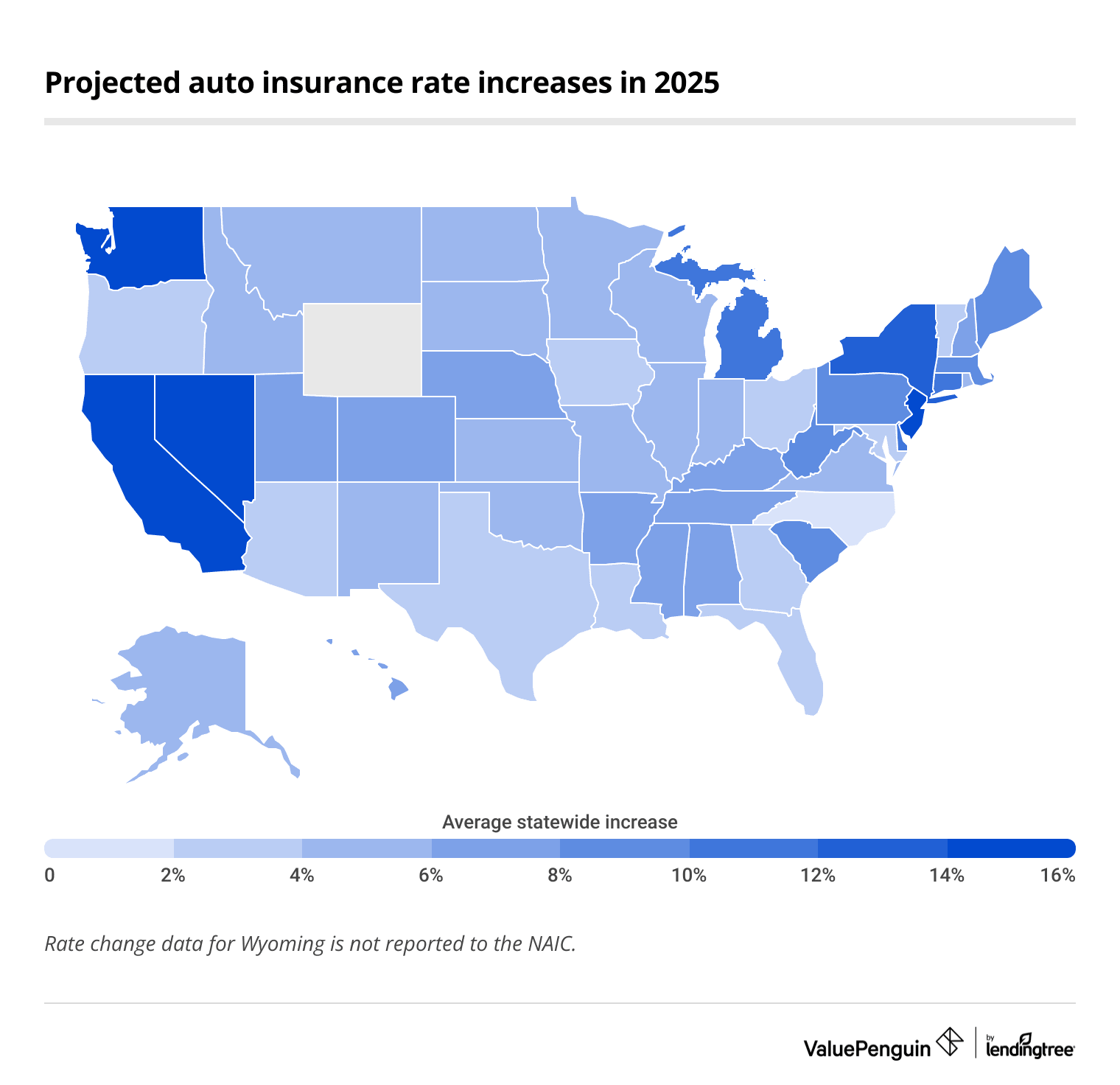

Average car insurance rate changes in 2025

Car insurance costs are expected to increase by 7.5% across the US in 2025.

While drivers across the country can expect to pay an average of 7.5% more in 2025, price jumps vary a lot by state.

New Jersey, Washington and California drivers can expect to see the biggest jumps the next time they renew. New Jersey and Washington have estimated increases of 17.2%, while California residents will see a 16.2% increase, on average.

Only one state — North Carolina — has an expected rate drop in 2025 (0.1%). That means NC drivers are the most likely to see no change, or even a slight drop, in their insurance rates next year.

The Bureau of Labor Statistics reported that people paid an average of 19% more for car insurance in 2024 than in 2023, though that also includes increased coverage amounts and higher vehicle replacement costs.

2025 rate increases by company

The rate increases drivers will face in 2025 can also differ by company. American Family is set to hike its rates the most among major insurers, with a massive 16.0% increase.

Meanwhile, USAA drivers can expect an average of 2.6% increase over the next year. Geico and Progressive are also raising rates only a small amount in 2025.

Insurer | Avg rate increase | |

|---|---|---|

| American Family | 16.0% |

| Allstate | 11.2% |

| Liberty Mutual | 10.2% |

| Nationwide | 9.7% |

| Farmers | 9.6% |

How much does a traffic violation increase car insurance costs?

Drivers with a traffic violation or accident could see an average car insurance rate increase of 53% in 2025.

Drivers in North Carolina are likely to see the highest cost increase after a road incident, with a typical increase of 146%.

DUIs are especially costly for North Carolina drivers, resulting in a typical cost of $591 per month after just one incident.

Pennsylvania drivers are likely to see the smallest increase, with a typical increase of just 35% after an incident on the road.

Car insurance costs after a ticket, accident or DUI

State | Rate hike | Ticket | Crash | DUI |

|---|---|---|---|---|

| North Carolina | 146% | $192 | $244 | $591 |

| California | 108% | $241 | $332 | $477 |

| Hawaii | 95% | $146 | $172 | $408 |

| New Jersey | 76% | $250 | $382 | $416 |

| Connecticut | 72% | $235 | $316 | $451 |

| Michigan | 68% | $332 | $359 | $631 |

Rate hike is based on the average price among one speeding ticket, at-fault crash or DUI, compared to the price of insurance for a driver with a clean record.

Cost of car insurance for the most popular new cars

The Toyota RAV4 and Honda CR-V are the cheapest new cars to insure in 2025.

The two cars each cost about $244 per month to insure, which is 16% less expensive than average among the most popular 2024 models.

The most expensive car to insure is the Tesla Model Y, at an average of $396 per month.

New cars generally cost more to insure than older models because they're worth more and it's harder to find replacement parts. However, new safety features like blindspot detection can offset that by reducing the chance that drivers get in a crash.

Cost of car insurance for top-selling cars

Car model | Monthly rate |

|---|---|

| Toyota RAV4 | $244 |

| Honda CR-V | $245 |

| Nissan Rogue | $270 |

| Honda Civic | $278 |

| Toyota Camry | $281 |

Electric car growth slows, while insurance rates compared to gas cars hold steady

While electric cars continue to grow in popularity, their insurance prices compared to gas cars have stayed steady. The top 10 EVs cost an average of $344 per month to insure — 23% more than the top gas-powered cars, or the same difference as last year.

Electric cars are expected to make up about a quarter of new car sales in 2025, per Cox Automotive.

The biggest new EV of 2024, the Tesla Cybertruck, is also among the most expensive. The average price to insure a new Cybertruck is $422 per month. That's the second-most expensive EV, behind only the Rivian R1S ($432 per month).

Teslas are typically very expensive to insure.

In general, electric cars made by legacy manufacturers like Ford and Volkswagen tend to be about 25% less expensive than those made by EV-only companies. This may be because replacement parts from these brands are easier to find, in addition to lower vehicle prices.

Cost of car insurance for popular EVs

EV model | Monthly rate |

|---|---|

| Volkswagen ID.4 | $240 |

| Ford F-150 Lightning | $283 |

| Hyundai Ioniq 5 | $316 |

| Ford Mustang Mach-E | $316 |

| Cadillac LYRIQ | $348 |

2025 car insurance trends

Inflation is down...

Inflation has fallen to just over 3% for the last half of 2024. A major driver of car insurance price hikes over the last three years was the cost of repairs, so falling inflation means insurance price increases may continue to slow.

Financing options are also improving, bringing down the overall cost of insuring a new car in 2025.

But tariffs may increase rates.

However, if President-elect Donald Trump goes forward with his plan to impose tariffs on imported goods, insurance rates may increase again.

About 60% of replacement car parts are imported from other countries. Higher parts costs mean higher repair prices, which would likely result in higher premiums.

Trump has posted on social media that he intends to cut car insurance rates, but there's not much he can do to directly influence prices. Insurance companies set rates in tandem with individual states, without input from the federal government.

How can I save money on auto insurance in 2025?

While the impact of inflation and regulation changes on car insurance in 2025 may be uncertain, how to save is not.

SHOP AROUND

The most important thing any driver can do to save money on their car insurance is to compare prices from multiple companies — at least five insurers, or more if you have a recent incident. That could save drivers more than $100 each month.

IMPROVE YOUR CREDIT SCORE

Insurers in almost every state use your credit score to set car insurance rates. A driver with good credit can bring their rates down from $341 to $175 per month compared to one with bad credit.

So paying your credit card on time and consolidating your debts will help you save each month on car insurance.

LOOK FOR DISCOUNTS

Insurance companies give you discounts for taking actions that make you less risky to insure.

Drivers in some states can also take a safe driving course to drop your rates, no matter which insurance company you have or whether you've recently gotten a ticket. For example, all drivers in New York can take an online course to save 10% on their insurance for three years.

Another effective discount is to bundle your home and auto insurance. That can save you between 11 and 24% among top insurers.

About this report

ValuePenguin has a mission to empower people with information and resources to help them make smarter financial decisions. Car insurance can be a difficult and time-consuming topic to understand. This report attempts to unmask some of the critical issues.

In crafting our analysis, we reviewed more than 20 million quotes for different drivers, adjusting for the factors that impact auto insurance premiums the most. We gathered rates from 45 insurance companies across the country since rates can vary widely by company.

Methodology

Auto insurance rate change data was compiled using RateWatch from S&P Global, which uses annual information from the National Association of Insurance Commissioners (NAIC).

Quotes are for a 30-year-old man who drives a 2015 Honda Civic EX with good credit and a clean driving record, unless otherwise noted. Quotes include the largest companies in each state from all available ZIP codes.

Rates for popular car models are from every ZIP code in Illinois and based on sales data from Cox Automotive through Q3 2024. All insurance quotes were gathered between October and December 2024.

ValuePenguin's analysis used insurance rate data from Quadrant Information Services. These rates were publicly sourced from insurer filings and should be used for comparative purposes only, as your quotes may differ.

Quotes are monthly costs for full coverage unless otherwise stated. Full coverage quotes include collision and comprehensive coverage, plus liability coverage and any others required by law.

Coverage Type | Coverage limits |

|---|---|

| Bodily liability | $50,000 per person/ $100,000 per accident |

| Property damage | $25,000 per accident |

| Uninsured / underinsured motorist BI | $50,000 per person/ $100,000 per accident |

| Comprehensive & collision | $500 deductible |

| Personal injury protection | Minimum when required by state |

About the Author

Lead Writer

Matt Timmons is a Lead Writer on the insurance team at ValuePenguin, where he writes in-depth and timely pieces helping find the right coverage for them.

He's covered insurance at ValuePenguin since 2018, specializing in auto and home insurance, as well as life insurance. He's paid special attention to the EV insurance market, where prices are much higher than for gas cars.

Before he started writing about personal finance, Matt wrote about professional skills and online tools at an e-learning company.

How insurance helped Matt

During freshman orientation in college, Matt's iPod was stolen off his table while he was eating lunch. Luckily, he'd bought a college insurance plan the day before and he had money to buy a replacement before classes started.

Expertise

- Auto insurance

- Home insurance

- Insurance rate analysis

- Life insurance

Referenced by

- CNBC

- Miami Herald

- Yahoo! Finance

Education

- BA, Wesleyan University

Editorial Note: The content of this article is based on the author's opinions and recommendations alone. It has not been previewed, commissioned or otherwise endorsed by any of our network partners.